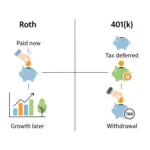

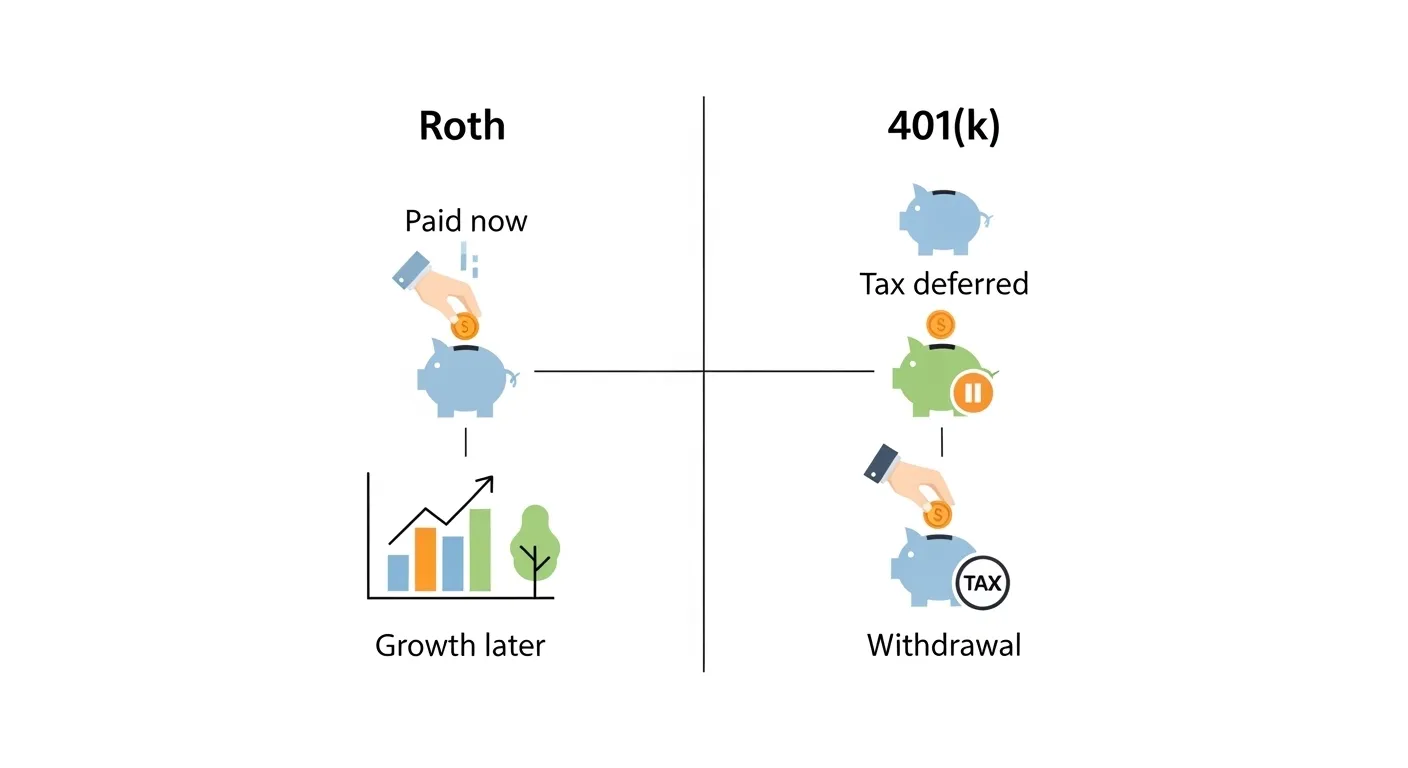

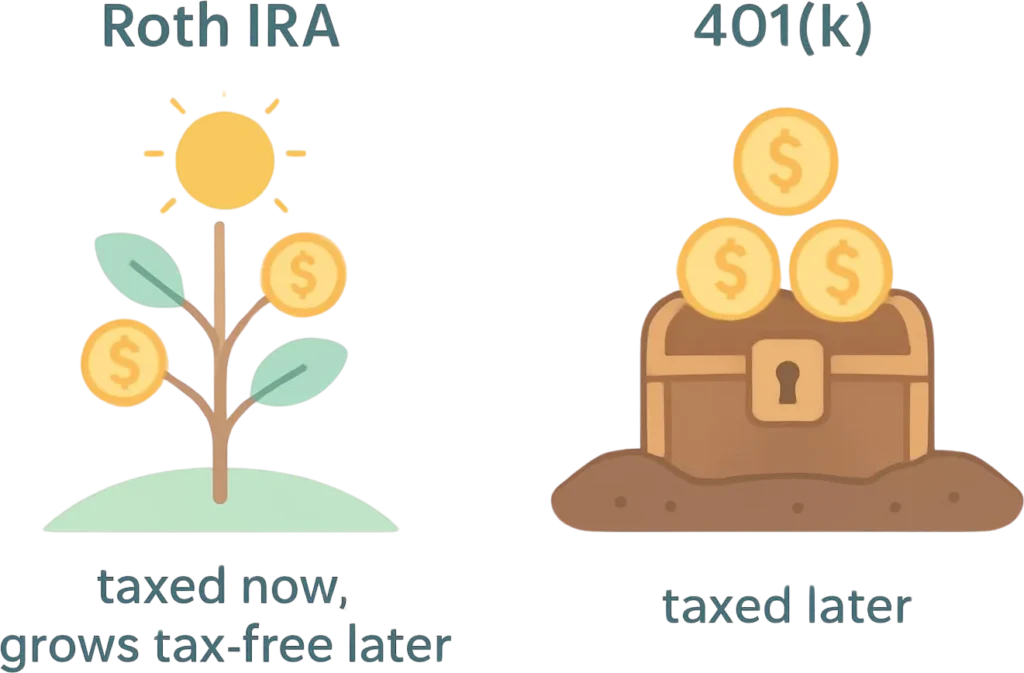

Roth is taxed now but grows tax-free later 💰, while 401(k) is taxed later when you withdraw 💼.

A young worker named Ali started his first job. On his first day, the company gave him a form. It asked if he wanted to save money in a Roth account or a 401k plan. Ali felt confused. Both plans were about saving money for the future. But they were not the same.

This small moment shows the difference between Roth and 401k. Many workers see these names in job documents. Yet they do not fully understand them. A Roth account usually means a Roth IRA, where money grows tax-free. A 401k is a retirement plan offered by employers.

Knowing the difference between Roth and 401k helps workers plan their future. The difference between Roth and 401k also affects taxes and savings. When people understand the difference between Roth and 401k, they can make smarter money decisions.

🔑 Key Difference Between the Both

The key difference is simple.

Roth: You pay tax now, but withdrawals later are usually tax-free.

401k: You save money before tax, but you pay tax when you withdraw it later.

🌍 Why Their Difference Is Important for Learners and Experts

Learners need this knowledge to manage personal finance. Experts such as financial advisors use it to guide people. Understanding these plans helps individuals save for retirement. It also helps society because financially secure citizens depend less on public support systems.

🔊 Pronunciation

Roth

- US: /rɔːθ/

- UK: /rɒθ/

401k

- US: /ˌfɔːr əʊ wʌn ˈkeɪ/

- UK: /ˌfɔː wʌn ˈkeɪ/

Now let us explore the difference between Roth and 401k step by step.

⚖️ Difference Between Roth and 401k

1. Tax Timing

Roth: Taxes are paid before saving.

Examples:

- A worker saves money after paying income tax.

- Retirement withdrawals are tax-free.

401k: Taxes are paid later.

Examples:

- Salary goes into the account before tax.

- Withdrawals in retirement are taxed.

2. Account Type

Roth: Usually an individual retirement account.

Examples:

- A person opens it independently.

- It is not tied to an employer.

401k: Employer-sponsored plan.

Examples:

- Companies offer it to employees.

- Contributions come from salary deductions.

3. Contribution Limits

Roth: Lower yearly limits.

Examples:

- Individuals save a smaller amount each year.

- The government sets strict caps.

401k: Higher yearly limits.

Examples:

- Workers can contribute more money.

- Companies may match contributions.

4. Employer Involvement

Roth: Usually no employer match.

Examples:

- Individuals contribute alone.

- No company contribution.

401k: Employers often match contributions.

Examples:

- A company adds extra money.

- Matching boosts retirement savings.

5. Withdrawal Rules

Roth: Qualified withdrawals are tax-free.

Examples:

- Retirement withdrawals have no tax.

- Contributions may be withdrawn earlier.

401k: Withdrawals are taxed.

Examples:

- Retirement income is taxed.

- Early withdrawal penalties may apply.

6. Income Limits

Roth: Has income limits for eligibility.

Examples:

- High earners may not qualify.

- Government sets income caps.

401k: No income restriction.

Examples:

- All employees can join.

- High earners can still contribute.

7. Flexibility

Roth: More flexible withdrawals.

Examples:

- Contributions can be withdrawn early.

- Some penalty exceptions exist.

401k: Less flexible.

Examples:

- Early withdrawals often face penalties.

- Rules are stricter.

8. Required Minimum Distributions

Roth: Usually no required withdrawals during life.

Examples:

- Funds can remain invested longer.

- People keep money growing.

401k: Requires withdrawals at older age.

Examples:

- Government requires minimum withdrawals.

- Taxes apply on distributions.

9. Investment Options

Roth: Often offers many investment choices.

Examples:

- Stocks and funds available.

- Individuals choose strategies.

401k: Limited options chosen by employer.

Examples:

- Pre-selected mutual funds.

- Fewer investment choices.

10. Long-Term Benefit

Roth: Good for future tax savings.

Examples:

- Tax-free retirement income.

- Ideal for young earners.

401k: Good for immediate tax relief.

Examples:

- Lower taxable income now.

- Employer matching increases savings.

⚙️ Nature and Behaviour of Both

Nature of Roth

Roth accounts focus on long-term tax-free growth. They are flexible and personal.

Nature of 401k

401k plans focus on structured retirement savings through employers.

❓ Why People Confuse Roth and 401k

People confuse these plans because both are retirement savings tools. They also appear together in financial discussions. Some companies even offer Roth options inside 401k plans, which makes the terms seem similar.

Difference and Similarity Between Roth and 401k

| Feature | Roth | 401k | Similarity |

| Tax | Paid now | Paid later | Both involve taxes |

| Provider | Individual account | Employer plan | Both for retirement |

| Contribution limit | Lower | Higher | Both allow yearly savings |

| Withdrawal | Tax-free | Taxed | Both used after retirement |

🎯 Which Is Better in What Situation?

Roth

A Roth account works best for young workers or people who expect higher taxes later. Paying tax now may be easier when income is lower. In the future, withdrawals are tax-free. This can help people keep more retirement money.

401k

A 401k plan is best for employees who want immediate tax benefits. It also helps when employers offer matching contributions. Employer matching acts like extra income. Many workers build large retirement savings through consistent 401k contributions.

🧠 Roth and 401k in Metaphors and Similes

Roth metaphor

Example:

- A Roth account is like planting a tree today and enjoying tax-free fruit later.

401k metaphor

Example:

- A 401k plan is like storing grain for winter.

🎭 Connotative Meaning

Roth

- Positive: future security, tax freedom

Example: - A Roth account promises tax-free income later.

401k

- Positive: structured saving and employer support

Example: - A 401k builds retirement savings step by step.

💬 Idioms or Proverbs Related

“Save for a rainy day.”

Example:

- She invests in a Roth account to save for a rainy day.

“Don’t put all your eggs in one basket.”

Example:

- Investors diversify beyond their 401k plan.

📚 Works in Literature

- The Wealth of Nations Economics, Adam Smith, 1776

- Rich Dad Poor Dad Personal finance, Robert Kiyosaki, 1997

- The Intelligent Investor Finance guide, Benjamin Graham, 1949

🎬 Movies Related to Finance or Wealth

- The Big Short (2015, USA)

- Wall Street (1987, USA)

- Moneyball (2011, USA)

❓ Frequently Asked Questions

1. What is the main difference between Roth and 401k?

Roth accounts use after-tax money, while 401k plans use pre-tax income.

2. Which plan has employer matching?

401k plans often include employer matching.

3. Which plan gives tax-free withdrawals?

Roth accounts usually allow tax-free withdrawals.

4. Can someone have both accounts?

Yes. Many people save using both plans.

5. Which plan is better for young workers?

Roth accounts are often better for young earners.

🌱 How Roth and 401k Are Useful for Surroundings

Roth and 401k plans help people build financial stability. When citizens save for retirement, they depend less on social support systems. These savings also support economic growth because invested money helps businesses and markets.

🏁 Final Words for Both

Roth represents tax-free future income and flexible saving.

401k represents structured retirement planning through employers.

Both play important roles in financial security.

🧾 Conclusion

The difference between Roth and 401k is mainly about taxes, contribution limits, and employer involvement. Roth accounts require paying tax today but allow tax-free withdrawals later. A 401k plan lets workers save before tax but requires tax payments during retirement. Both plans help people build financial security for the future.

Understanding the difference between Roth and 401k allows individuals to choose the right plan based on income, tax expectations, and career stage. With proper planning, these accounts can create a strong financial foundation for retirement.

Read more about!

Difference Between Nerd and Geek: Simple Guide

I have studied from Carl Woese, an American microbiologist who revolutionized biology by discovering the domain Archaea. Through his work, I understand how the classification of life was reshaped, clearly distinguishing archaea from bacteria based on genetic differences.